Claret Capital Partners (“Claret”) has been providing growth funding to technology and life sciences companies for over 13 years. In that time, our funds have backed more than 190 companies and deployed over €1.2 billion in capital, making us one of the most experienced players in the European growth lending space. We’ve seen the weird, the wonderful, and everything in between across the European venture ecosystem. Over the years, our team has also analysed data from thousands of companies and learnt a lot about what works – both for us and for the borrowers – and just as importantly, what doesn’t.

To give you a sense of the volume of companies we’ve looked at: in the last 12 months alone, (since Jul-25) we have reviewed over 1,000 businesses and issued term sheets to around 60 – a 6% hit rate. The good news is however, that there are clear steps you can take to increase your chances of success, get better terms, and assess if we’re the right fit for you.

While this piece focuses on raising venture debt, a lot of the advice applies to equity raises too.

- Understand the Product

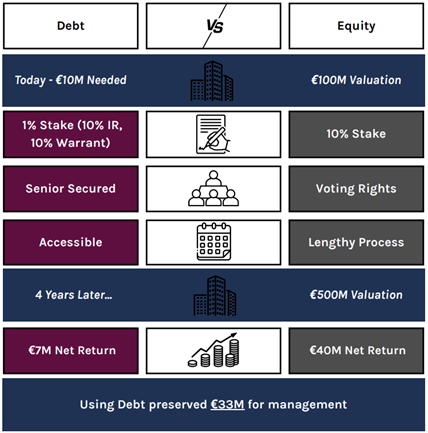

Venture debt can be an excellent way to avoid dilution and lower your cost of capital. If you’ve studied finance, this won’t be news—but here’s a quick example:

Source: Claret Capital Partners

While this sounds great, and while debt is cheaper, it is not as flexible: the obvious fallback is that when things don’t go as well, the lender still expects repayment. That’s why debt isn’t always the right tool for businesses that have little visibility of revenues or performance into the next 12 months.